The financial trap no one talks about

The slow, quiet creep that sneaks up on you.

Over the past month alone, I’ve been to a concert, a comedy show and even splurged for “Sinners” — despite today’s outrageous movie theater prices.

It’s the most this old man has been outside in a while.

But that’s just the beginning.

In nearly the same stretch, I put down a deposit for a family vacation, booked a business conference, purchased two pairs of shoes, picked up high-end body lotion, grabbed a few books and — because I apparently have no self-control — added more Minnesota Vikings gear to my already overflowing collection.

No surprise my spending has spiked.

A recent root canal isn’t the only thing that’s blown up my credit card balance.

The harsh truth?

My spending has increased every month this year, peaking last month at a personal high.

Sure, I can point to responsibility: recurring legal fees that started early this year, an expensive and unexpected dentist bill and more costly car repairs.

But deep down, I know I’ve loosened my grip. I’m spending more freely largely because I can.

And that mindset? It’s one of the fastest killers of wealth.

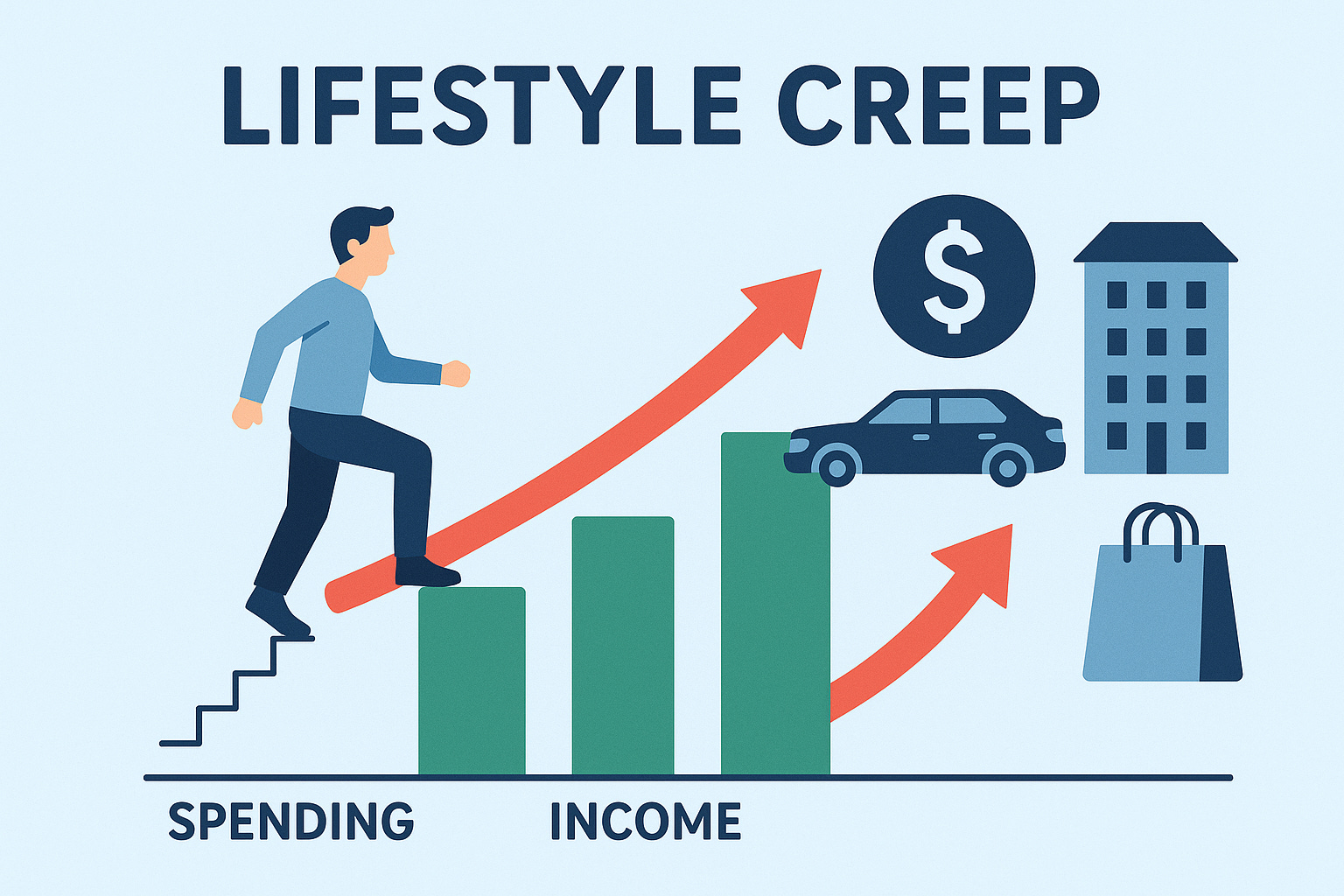

It’s called lifestyle creep, or lifestyle inflation, and how it works is simple: when we earn more, we tend to spend more.

It doesn’t hit all at once, and it’s rarely anything dramatic. Just a slow parade of “treat yourself” moments that somehow transform into non-negotiables.

At first, you don’t see anything wrong with going to the Anthony Hamilton concert. Tickets to legendary comedian Bruce Bruce? They won’t break the bank. But then, why stop there? Might as well support Ryan Coogler and Michael B. Jordan on the big screen, too.

Naturally, I also needed nicer shoes, a new watch battery and to renew my TSA PreCheck.

The funny thing?

My income hasn’t increased, but I keep hitting “buy.”

A few life changes quietly made it easier to open my wallet wider.

The biggest was paying off my car and becoming a two-income household at the end of 2024.

Then, when our house hunt went on hold, more money freed up. I wasn’t about to let our savings sit idle while life passed by. Instead, I chose to spend on experiences that mattered.

This isn’t reckless spending, it’s intentional living.

I’m at peace with this bout of lifestyle creep because, for the first time, my money is flowing where it really matters — into investments that build real wealth.

So while my spending has grown, my long-term goals haven’t slipped. That balance brings me confidence but also comes with a warning.

Even the best intentions can quietly erode your savings if you’re not careful.

The trick isn’t just making more money.

It’s keeping your lifestyle in check while you build wealth.

How to use credit cards wisely and avoid debt

A young professional recently asked me how to use a credit card, which caught me off guard.

Transform your finances today with this essential tool

The most valuable financial weapon in my arsenal comes from my primary credit card — the spending planner.

This was such a good read. You owe it to yourself to be honest about your struggles so you can address them face to face. You got this!

Some lifestyle creep is okay as long as it is balanced by savings or by more income. I generally think about it as a percentage of net income.