What happens when you finally go outside?

A last-minute date, a packed rooftop and another $4,000 month.

On the final Friday in May, I planned a last-minute date that couldn’t have gone much better.

But before the evening truly began, I found myself distracted by something else entirely.

Driving to the hotel rooftop where we had reservations, I passed one crowded scene after another. Restaurant patios were overflowing. Rooftop bars were packed shoulder to shoulder. Groups wandered the streets looking for the next place to go, the next drink, the next experience.

For a moment, I couldn’t believe my eyes.

With everything so expensive these days, I found myself wondering where people get all this money. How can they afford it? And, in some cases, I know the answer is that they can’t — but that doesn’t necessarily stop them.

If you judged the economy solely by what I saw that night, you’d never guess the country or its citizens were under any financial pressure at all. There were no visible signs of restraint. No indication that inflation, housing costs, student loans or credit card balances were weighing on people’s minds.

Then again, that’s what happens when you don’t go outside.

It’s easy to develop a distorted view of reality when most of your time is spent at home, working, reading, or scrolling through headlines that paint a picture of economic anxiety. The real world often looks very different from the one described in surveys and statistics.

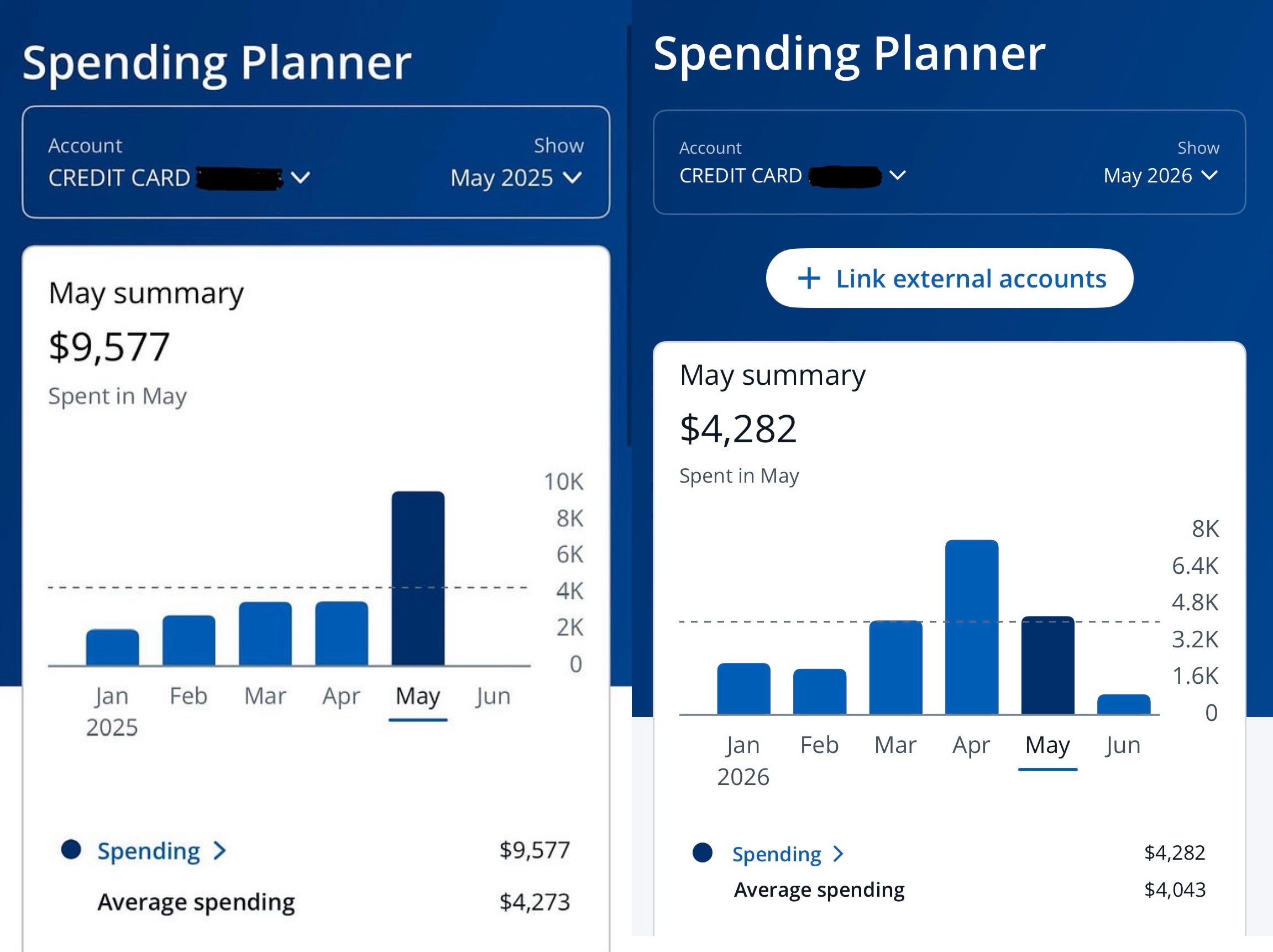

Judging by my own credit card statement, though, you’d think I was right there among the big spenders.

Most of my purchases go on a credit card so I can rack up airline points. A few essentials — like rent, gas for my vehicle and apartment, electricity and my $10 monthly gym membership — are paid separately. Tracking expenses this way lets me monitor spending in real time, and each month I share my progress, for better or worse.

May marked the third consecutive month that I spent more than $4,000.

I can’t remember another stretch when that has happened. Tracking expenses month over month has become one of my favorite financial habits because it helps provide context. Numbers by themselves can be alarming until you compare them against prior periods.

Looking back at last May, for example, reminds me that this year’s spending isn’t nearly as dramatic as it first appears. Last year featured a root canal and the kind of dental bill that makes almost every other expense seem reasonable by comparison.

The biggest category in May was professional services, which accounted for 23 percent of my spending, or $1,001. That figure comes after professional services made up nearly half of my April balance. May’s total included a $35 apartment application fee, along with attorney’s fees that are starting to pile up.

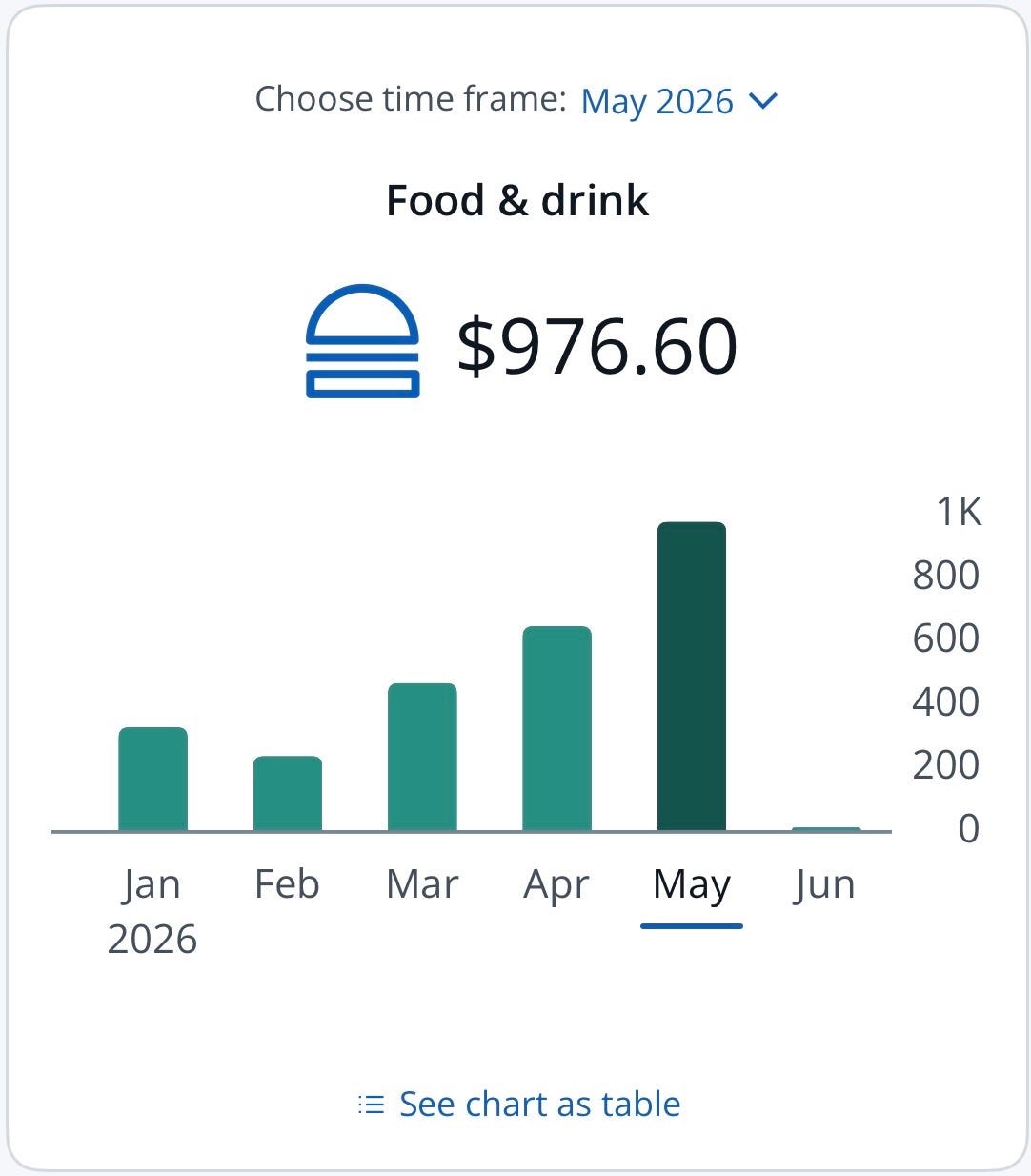

The category that stood out most, however, was food and drink.

At $976.60, it was my highest total of the year.

Truthfully, the explanation is simple: I’ve been dating more.

Meals, drinks, coffee shops, rooftop bars — those costs add up quickly. While it’s not exactly a budget-friendly development, I’m surprisingly at peace with it.

One of my goals has been to spend less time sitting at home and more time engaging with the world around me. Dating has accomplished that, even if it comes with a larger restaurant tab.

Not every increase was intentional. Subscriptions have started creeping back up as well. I added The Wall Street Journal for $8 per month and Netflix for $9.91 per month. The Journal is staying. Netflix, however, lasted only a month before I canceled it. It didn’t take long to realize that I simply don’t have enough time to Netflix or chill.

Otherwise, everything continues to run smoothly.

Still, the first half of the year has followed a familiar pattern. Just when my budget seems settled, I get hit with more large and unexpected bills that force an adjustment.

It’s a reminder that personal finance is never perfect.

And judging by the crowds I saw that Friday night, we’re all figuring it out in real time.

The boring stage of wealth building

There’s a phase in every successful journey that doesn’t look impressive from the outside.