Back in the same storm

My midyear spending looks nearly the same as last year.

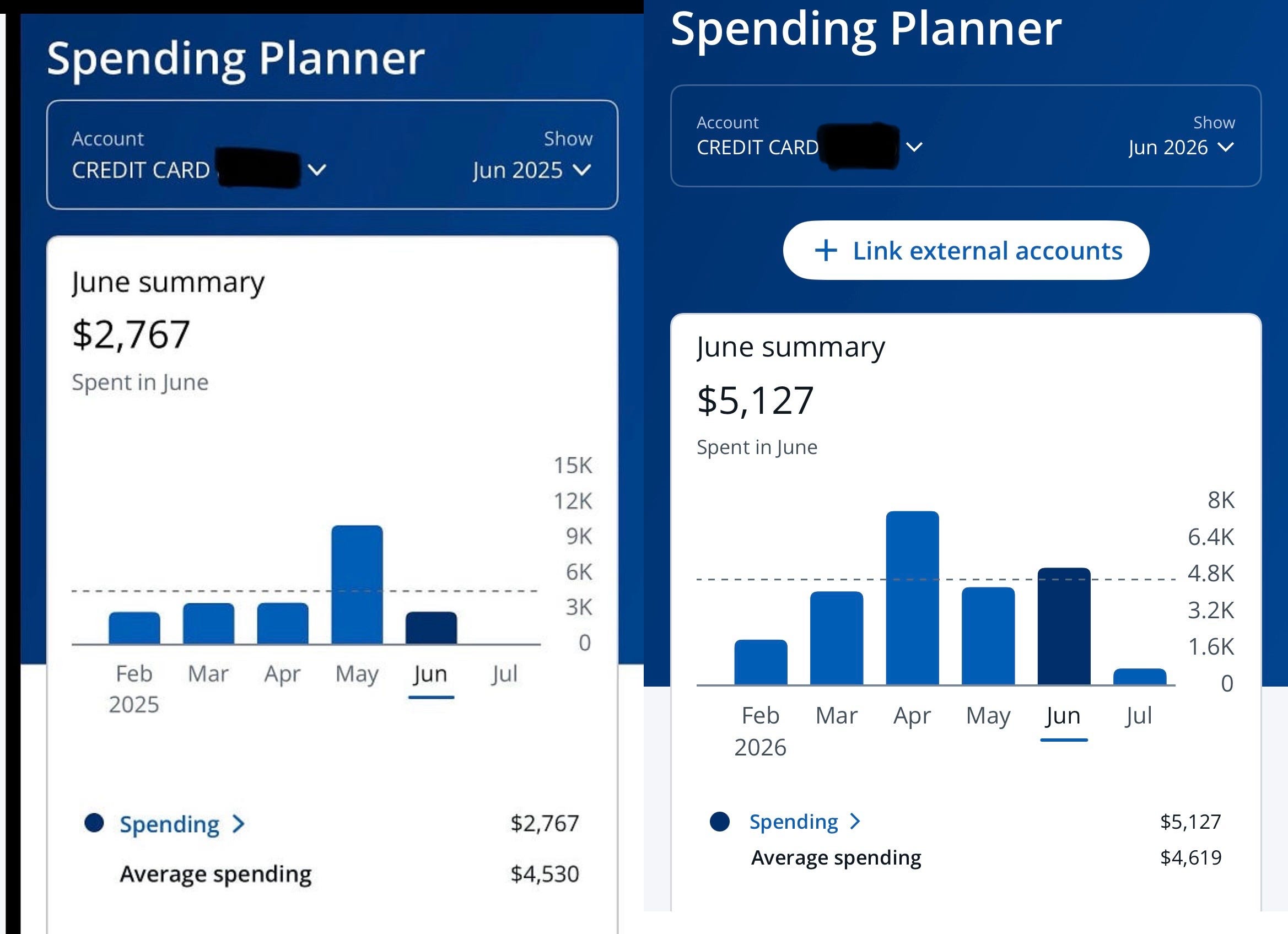

June marked my fourth straight month of spending more than $4,000.

I keep waiting for this stretch to let up, but instead it feels like every time I look up, another expense is headed my way.

It feels like everything is hitting me at once. And the biggest bugaboo is a familiar one.

Since April, my professional services category has accounted for 49%, 23% and now 35% of my monthly spending. It has completely reshaped my budget, and at times, it feels like a bomb has been dropped on my finances.

Then, over the holiday weekend, road debris left my vehicle with minor body damage. Now I’m staring at yet another bill that needs immediate attention, whether I decide to file an insurance claim or pay out of pocket.

It’s amazing how quickly financial pressure can cloud your thinking.

Vision gets blurred. The goal gets distorted.

Fatigue flew out the window a long time ago. I’m nearing exhaustion as setback after setback keeps arriving.

I’m feeling the weight of constantly having to adjust.

What’s worse is watching so much money leave your accounts after spending years being intentional with every dollar.

Because I invest as aggressively as I do, there isn’t much room in my budget for superfluous spending. So when the money that remains has to go toward expenses I’d much rather avoid — and those expenses are large enough to force me to tap my freedom fund while threatening my investing strategy — the situation can’t help but feel like a storm.

Most of my purchases go on a credit card so I can rack up airline points. A few essentials — including rent, gas for my vehicle and apartment, electricity and my $10 monthly gym membership — are paid separately. Tracking my expenses this way lets me monitor my spending in real time, and each month I share the numbers, for better or worse.

I’ve had to bite the bullet and pull from my freedom fund, the safety net I worked so hard to build.

This is where things become uncomfortable.

My freedom fund exists for seasons like this, but that doesn’t make using it feel any better. When this passes, rebuilding it moves to the top of my priority list.

This season has also exposed a habit I hadn’t fully acknowledged before. The more my bills pile up, the more tempted I am to splurge.

My only explanation is that I abhor watching so much money leave my accounts without enjoying at least a little of it myself. It’s not the healthiest financial instinct, and June reflected it.

I spent $629.19 on food and drink — the third straight month I’ve eclipsed $600 and the second consecutive month it ranked as my second-largest spending category. If there were ever a time to tighten that up, it’s now.

As overwhelming as this season feels, perspective still matters.

Despite the string of setbacks, my average monthly spending through the first six months of 2026 is only $89 higher than it was during the first half of 2025.

Considering everything that’s happened, that number surprised me.

I expected this year’s spending to be much higher at the halfway point, but the close numbers reminded me I went through something very similar last year too.

I’m disappointed to see the pattern repeat itself another year — and likely more consecutively than that.

The storm is real, and so is the preparation that came before it.

My freedom fund is doing exactly what it was built to do, even if I don’t know when this stretch will pass.

I’ll get through it.

What happens when you finally go outside?

On the final Friday in May, I planned a last-minute date that couldn’t have gone much better.